R&D Tax Relief

R&D Tax Relief - Does my project qualify?

What counts as Research & Development to HMRC?

To HMRC, qualifying R&D is when a project seeks to achieve an advance in science or technology by resolving scientific/technological uncertainty. This is an advance in the entire field of science or technology that you operate in.

- These advances can be tangible (i.e. improved and/or new product or processes) or intangible (i.e. new knowledge or cost improvements).

- However, something is not appreciably improved if it simply brings your product or offering in line with overall knowledge or capability in science or technology, even if it is new to your company. If you are using third-party technology, or are building features & products that competitors have had for years, this makes it less likely that your project qualifies as R&D.

As a result, in your R&D claim, you can only claim for projects that try to advance the whole technological field that you are in.

HMRC's examples of Research & Development

- Searching, evaluating & applying research findings.

- Searching for new materials, devices, products, processes, systems & services.

- Formulating, designing, evaluating & selecting new or improved materials, devices, products, processes or systems.

- Designing, constructing & testing pre-production prototypes & models.

- Designing, constructing & testing new materials, devices, products, processes, systems & services.

- Designing tools, jigs, moulds & dies involving new technology.

- Designing, constructing & operating a pilot plant that is not of economically feasible scale for commercial production. But if the same plant were of economically feasible scale for commercial production then it does not qualify for R&D.

How to evaluate if your projects meet these definitions for R&D?

Your work can be innovative, creative and not meet HMRC’s definitions of R&D for tax purposes. Some questions to ask yourself are:

- Are the features, products, services, processes & materials commonly used & available anywhere? Are they commonly used & available in similar business contexts?

- What is the scientific & technological baseline in your field & are you advancing it beyond this global baseline?

- Would your competitors have these features/products or comparable features/products?

- Was your project led by HMRC's definition of a ‘competent professional’? If not, then it will not qualify as R&D.

- If you did achieve an advance, was it an 'appreciable improvement' or is it a negligible advance?

- At the start of the project, would an experienced professional in the field have known if the project was technologically feasible & how to achieve it? If the answer here is yes, then there wasn't uncertainty to resolve and the R&D isn't qualifying.

Which stages of your project count as qualifying R&D spend?

R&D starts when you begin to ‘resolve the scientific/technological uncertainty’ and ends when the uncertainty is resolved.

What counts as qualifying R&D spend?

- Researching alternatives to your products - Unlikely (not directly related to resolving scientific/technological uncertainty).

- Evaluating commercial viability and costings of your project - No (not directly related to resolving scientific/technological uncertainty).

- Selling your project to your first customers - No (not directly related to resolving scientific/technological uncertainty).

- Developing a prototype to test internally, including the creation or adaption of software, testing designs etc - Yes (directly related to resolving scientific/technological uncertainty).

- Getting patents or building commercial production facilities - No (this is a commercial expense, not directly related to resolving the scientific/technological issue).

- Capitalised software development expenditure directed towards resolving technological uncertainty - Perhaps (if capitalised on Balance Sheet as a tangible asset this won’t count for R&D. If capitalised as an intangible fixed asset it may possibly qualify).

- Capitalised machinery, equipment, land or buildings - No (as above, if capitalised on Balance Sheet this won’t count for R&D. This expenditure may qualify for R&D Allowances (RDAs) but shouldn’t be included in your R&D claim).

- Expensed software development towards resolving technological uncertainty - Yes (the portion directly related to resolving the technological uncertainty).

- Any expenses incurred in the ordinary course of business such as Rent, Staff Training, Storage & Cleaning - No (unless these expenses are directly related to resolving the technological uncertainty, they will not qualify).

- Utilities such as water fuel & power - Perhaps (if related to the R&D).

- Planning activities related to project work - Perhaps (Expenditure on researching commercial, financial, marketing or legal aspects is explicitly non-qualifying but some planning can qualify)

- Essential indirect support activities such as administration and security, maintenance of equipment, leasing of laboratories - Yes (if these are qualifying indirect activities which are essential to the resolution of the technological uncertainty).

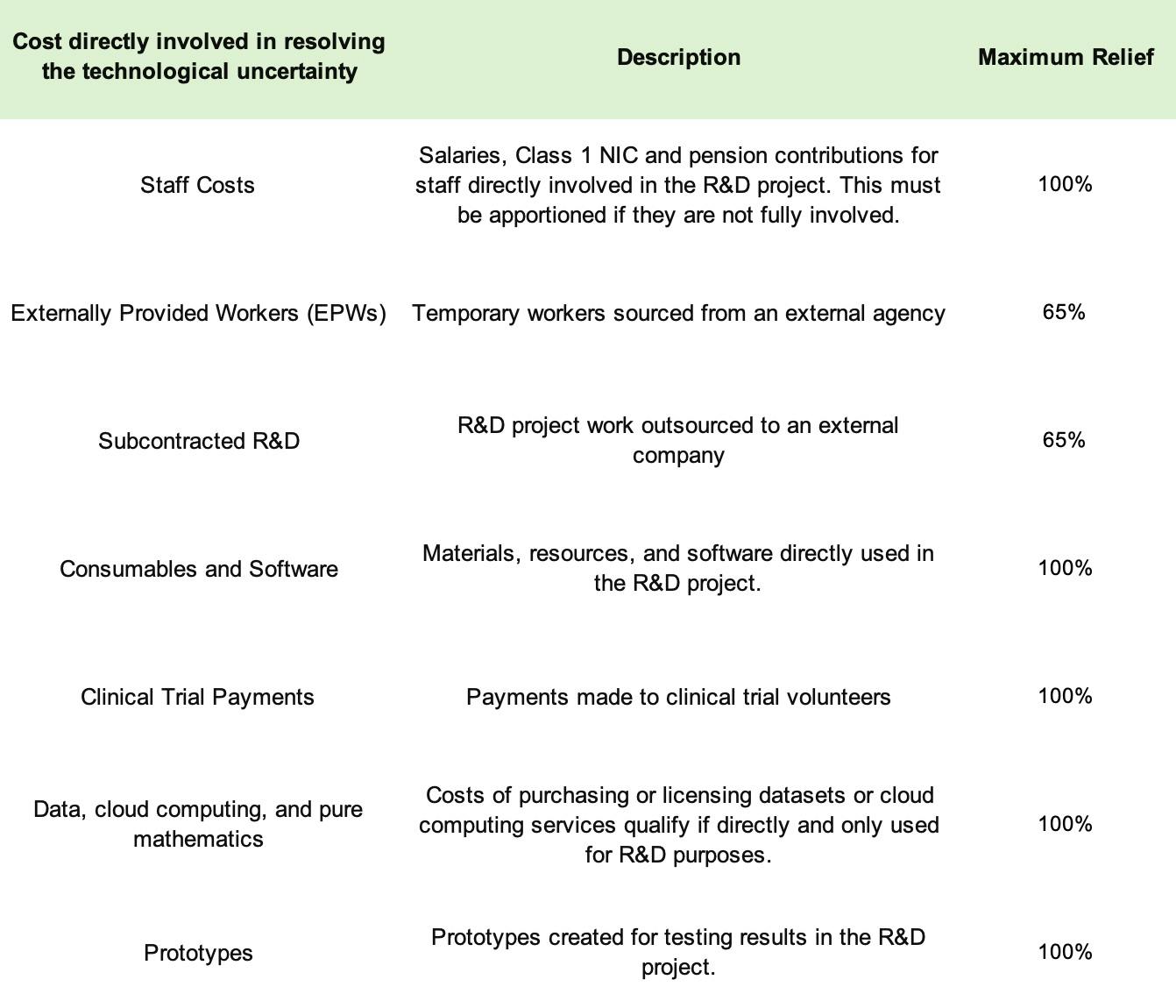

Potential Qualifying Costs

Practical Qualifying Relief

- Imagine that you have one software engineer working on a project for 6 months that you believe is qualifying R&D spend.

- Allocating 100% of their salary for that period to R&D work stretches credulity. This would imply that every second of every day for 6 months was spent on ‘resolving technological uncertainty’ rather than fixing bugs, maintaining infrastructure, and joining irrelevant meetings. In practice, it’s likely that 60% of their time was spent on R&D for the 6 months, even if it was their mainstream of work and therefore 30% of their total annual salary would be qualifying.

- Similarly, on cloud spending, any cost that is associated with running your day to day service isn’t qualifying. If you trained a custom AI model that was used commercially, the cloud cost to train the model could be qualifying, but the cost of running the service afterwards would not qualify.

- In practice, making claims for 100% of annual costs stretches credulity. When HMRC investigates R&D claims, this is a common line of their enquiry.

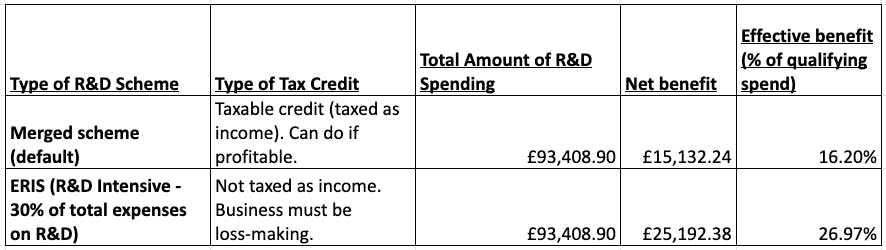

Is it worth making a Claim?

- The following worked example shows a situation, where you had one engineer earning £100,000 per year and they spent 80% of their working time on R&D qualifying work.

- The total staff costs would include Employer National Insurance & Employer Pension contributions and lead to the following R&D qualifying spend & tax credit to the business.

Your R&D Project Claim

- How many (if any) and which projects meet the definition of R&D?

- How long did the projects last and which stages of the project count as R&D? Whose time counts as R&D? What % of that person’s time was reasonably on R&D (being prudent on estimates to avoid overclaiming)?

What to include in the Project Report?

HMRC demands that you explain why & how your projects count as R&D, but also require that you explain this in terms that a layperson would understand. When describing your project and why it qualifies, these are the key questions to address:

- What was the advance in science or technology that you developed? If you are claiming to have achieved an advance, what quantification proves it is an advance or is it literally the first example of a 'thing' in the world?

- How did you establish what the current 'baseline' in your field was? HMRC may cite what is currently available commercially, what is available open source & what is available according to public knowledge.

- What was the particular area of scientific or technological uncertainty that needed resolving? This uncertainty must relate to the field, not just to your company's uncertainty. What is the uncertainty in the field that you resolve?

- Which field of science & technology did you advance & how did the project go beyond the current state of knowledge in the field?

- Who did the work, what were their qualifications & are they a highly qualified ‘competent professional’ according to HMRC definitions? - HMRC guide

- When did you overcome the uncertainties and have you clearly described the experimental and investigative methods used? Have you acknowledged any failures or unexpected outcomes in your process of resolving the uncertainty?

- Which activities & spend in the project met the definition of R&D for tax and is therefore qualifying?

- Have you clearly differentiated between commercial activities and R&D activities?

Key Definitions to HMRC

Advance in science or technology: means an advance in the knowledge or capability within a given field of science or technology. This can be tangible (i.e. new product) or intangible (i.e. new knowledge). It is not necessary for the advance to have been achieved; unsuccessful projects can still qualify for R&D relief.

Scientific or technological uncertainty: exists when knowledge of whether something is feasible is not readily available can cannot be easily deduced by a competent professional.

Competent professional: is someone with significant expertise in the field in which you are conducting R&D. They must have a recognisable track record. A competent professional must be employed in the R&D project.

Methodical experimentation: HMRC requires that companies experiment methodically. ‘Stabs in the dark’ will not qualify for R&D relief. Ensure to record results, assess progress then try another solution etc.

Appreciable Improvement: Essentially, your R&D project has to aim to substantially improve a product or service, rather than just ‘upgrade’ an existing version. This is something that would be recognised by a competent professional in the field as a genuine ‘non-trivial’ advancement.

After Your Claim

Usually, HMRC will review your claim and either approve it or decide to open an enquiry into whether the projects were R&D for tax and if the calculated amounts are correct. In the Individual & Small Business Compliance R&D team, you largely deal with a mailbox and not a single case worker who is an expert in your area. HMRC will ask for very detailed information lists asking you to elaborate on things like whether the projects meet the definitions of R&D, whether any R&D took place, what the start & end dates for the R&D were, what the qualifying costs were, if the %’s allocated were correct and whether anything is included that shouldn't have been allocated.

You can respond to these queries yourself, but this is time consuming for you. If you choose to use advisors to support you, this costs thousands of pounds. After around 3 rounds of information requests, HMRC will issue a closure notice saying there is or isn't R&D present. If they say there isn't R&D present, then you will have to repay any credit and can get penalties calculated based on the claim amount (30% is a common benchmark).

We can help talk you through all of the above points when submitting your R&D tax claim. While we do not offer tax advice, we will lay out all of your options and help you make the best decision for your business. Book in a call with one of our experts here.

What to do during the year?

Your R&D claim is submitted alongside your Corporation Tax return, so you don't need to do any calculations until year end. The only thing that may be worthwhile during the year is tracking which qualifying R&D projects you are working on and tracking how much time the employees & competent professionals are spending on each project by month to support you tracking the R&D calculation at year end. We've put together a template for you to do this here.

New content every Monday

No spam. Unsubscribe anytime.