Revenue-based financing

Introduction to the pros and cons of revenue-based financing

Revenue-based financing (RBF) has become an increasingly popular option among eCommerce and SaaS businesses. Some of you can probably tell by the number of emails and cold calls you’re getting from RBF lenders.

It has been marketed as a quick way to get working capital without diluting equity and keeping full control of your business. Compared to traditional bank loans, there are usually no personal guarantees, and getting approved is easier. Most importantly, revenue-based financing loans are repaid as a percentage of daily revenue rather than a fixed amount, which puts less stress on margins during weeks of lower revenue.

That looks great, but what isn’t always made clear is that despite all these benefits, the total cost of your borrowing for a year—often referred to as APR—of a revenue-based loan is typically higher than the APR of a traditional line of credit. Although, at first glance, the fee rate might be lower than the interest rate of a traditional loan, this is comparing apples to oranges.

So, let’s examine RBF loans to understand their pros and cons and when they are good options.

Standard revenue-based financing example

For example, let’s say you’ve been loaned £100,000 for a 5% fee with a 10% repayment percentage of gross revenue until the loan plus fee is paid back.

With a standard revenue-based finance loan, your repayment will look something like this:

- Month 1: sales of £50,000 and repayment of £5,000

- Month 2: sales of £90,000 and repayment of £9,000

- Month 3: sales of £60,000 and repayment of £6,000

This repayment schedule will continue until you fully repay the loan plus the fee. When revenue increases or drops, your repayments change accordingly, meaning your monthly cash flow is never negatively affected by a fixed high repayment amount.

Again, this repayment flexibility can be very advantageous, but it typically comes at a price.

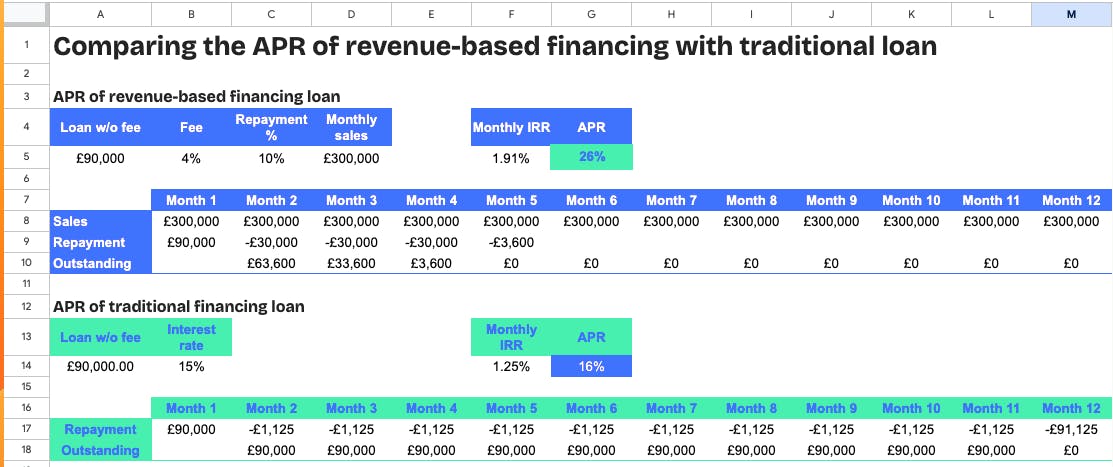

Comparing the cost of revenue-based financing versus traditional loans

You should not compare the loan fee with the interest rate when comparing RBF loans to traditional loans. Rather, we should calculate the annualised cost of your borrowing for both loans and compare those to each other.

Revenue-based loan example:

- Loan amount: £90,000

- Loan fees: 4% of loan amount

- Repayment: 10% of monthly sales

- Monthly sales: £300,000

Based on these numbers, the APR is 26%

Traditional bank loan example:

- Loan amount: £90,000

- Interest rate: 15%

Based on these numbers, the APR is 16%

In conclusion, even though the revenue-based fee of 4% looks lower than the 15% interest rate, when annualising both loans and comparing like for like, the revenue-based loan is almost two times more expensive.

But why then pick the RBF loan?

The main reason is that revenue-based lenders tend to understand digital businesses better and can underwrite you, whereas a traditional bank might not be able to provide you with a loan. This is specifically the case for earlier-stage businesses without a multi-year track record of sustained revenue and growth.

Below, I go into a few more benefits of RBF, but before doing so, let’s ensure we understand all relevant definitions well.

Typical terms and definitions

To determine whether a revenue-based loan is suitable for you, it’s important to understand the key components of an RBF loan:

- Loan amount: The investment size or principal is the actual loan you receive, including the fees and the total amount you will have to pay back. This is typically capped at 3x of your monthly revenue or up to ⅓ of annual revenue for seasonal businesses and ranges from £30k to £3M in check sizes). Sometimes, it is called the capital amount, disbursed amount, or funds provided.

- Fees: 2-10% of the loan amount must be paid back on top of the loan.

- Repayment percentage: 2-10% of revenue. It varies widely depending on the lender.

- Repayment schedule: daily, weekly, monthly or quarterly.

- Collection period: Also called the payoff period, this is the estimated duration of the loan before it is fully paid back.

- Grace period: duration before repayments start – 0 to 12 months.

- Eligible sales: Lenders can use gross revenue, net revenue, or gross profit to calculate repayment based on revenue. Understanding how they define revenue is important for calculating how much it affects your margins.

- Financial reporting: Lenders typically ask for access to your P&L, balance sheet, and cash flow statements, as well as connections to your live bank feed and payment providers.

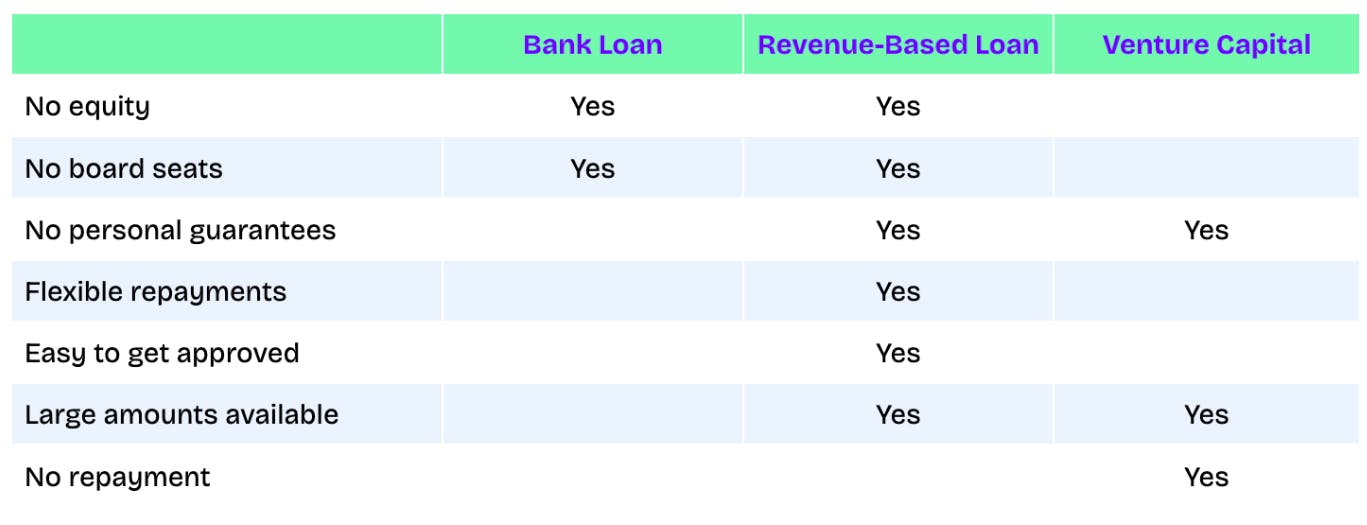

- Personal guarantees: none.

- Equity warrants: none.

- Board seats: none.

- Equity: 0%.

Which businesses are a good fit for revenue-based financing?

From a financial perspective, the following criteria make a business suitable for an RBF loan:

- Profitability: Lenders prefer EBITDA-positive businesses to minimise the risk of a business defaulting on the loan.

- Revenue: Depending on the lender, the minimum revenue criteria is usually £10k+ in monthly recurring revenue.

- Revenue growth: 30%+ annual

- Gross margins: 40%+

- Financials: 6+ months of trading with a proven track record of growth and sales

- Debt: no outstanding debt.

- Credit facilities: no access to standard credit facilities with low fixed fees. Even though I calculated earlier that a standard loan can have lower APRs, these loans aren’t always available for early-stage businesses.

In general, RBF loans are commonly used by early-stage digital businesses with a growing positive net cash flow that cannot yet obtain a traditional credit facility. Most eCommerce businesses use RBF to either shorten their cash conversion cycle (e.g., be more aggressive with marketing) or increase inventory volumes (e.g., run out of stock less frequently). Other purposes are less common and potentially less suited.

What to keep in mind with revenue-based loans?

When receiving a loan offer from a lender, try to negotiate more favourable terms. It is a very competitive market, and there’s often room to provide you with a better deal. I’ve also listed more general points to assess whether a revenue-based loan is the right choice:

- Start of repayment: RBF loans are frequently used to purchase inventory, so you may find yourself repaying the loan while awaiting the arrival of the inventory. Negotiating a delayed start for repayment could offer the necessary flexibility in such circumstances so that you do not end up repaying a loan you haven’t even benefitted from.

- Balancing working capital: It is important to balance loan spending between inventory and marketing. You can get in trouble when ordering too much inventory without having cash available to market it. Or, the other way around, a large percentage is spent on an experimental marketing channel (e.g., your first TV ad campaign) that might not bring the expected results.

- Fluctuating payment schedules: The downside of fluctuating repayment schedules is that it becomes hard to make financial projections. For easier financial planning, consider making fixed monthly payments instead of variable payments based on revenue.

- Impact on profit margins: The RBF loans directly eat into the gross margins every month, and thus, your business needs sufficient margins to support this. If margins are low, the repayments will directly affect the business's growth potential, and it is possible to end up in a situation where you depend on larger loans to grow rather than reinvest profits.

- Fees and penalties: Avoid origination fees, late payment penalties, and early repayment fees.

- Early repayment terms: Negotiate favourable terms for early repayment, including any associated fees or discounts. This can help you manage costs if your revenue increases substantially, especially for very seasonal businesses.

- Consider multi-draw advances: When you do not need a large lump sum payment upfront, consider negotiating to split the loan amount into multiple smaller amounts that you can call upon later. This lowers your repayment at the start and allows you to access additional capital later.

- Alignment with business cycles: Align payment schedules and terms with your business cycles, particularly if your revenue is seasonal. This can help manage cash flow more effectively as you increase your monthly repayment percentage during the months with higher revenue and profits.

Hopefully, this has given you the right guidance to assess whether your business is suitable for a revenue-based finance loan and how to negotiate better terms.

Remember that this, or any other online article for that matter, should not be taken as financial advice and will depend on individual circumstances. Discussing your unique business context with your financial advisors is always best. If you’re looking for an accountant to discuss your business, then do reach out to us.

New content every Monday

No spam. Unsubscribe anytime.